NBIS: The $8 Billion ARR Moonshot—Execution vs. Expectations

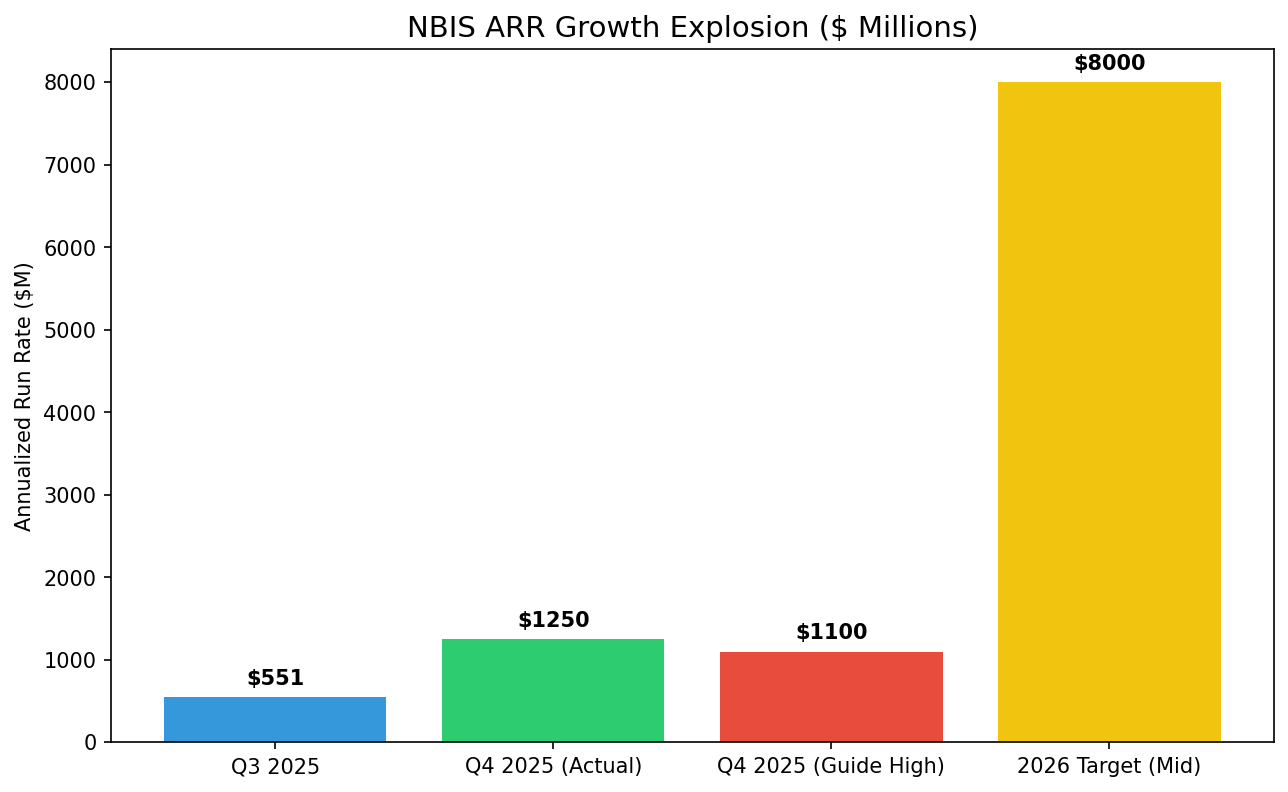

Following the Q4 2025 earnings release, Nebius Group (NBIS) has transitioned from a speculative spinoff to a verified execution leader in the AI Cloud space. While the headline revenue missed slightly due to timing, the Annualized Run Rate (ARR) reached $1.25 billion, smashing the upper end of management’s own guidance ($1.1 billion).

1. The "Meta-Metric": ARR Velocity

The most significant takeaway from the recent quarter is the speed of monetization. Reaching $1.25B ARR means that December revenue was approximately $104M.

Key Catalyst: The $23 Billion Backlog

NBIS isn't just building data centers; it's fulfilling a massive, high-margin backlog:

- Microsoft Deal: $17.4B over 5 years.

- Meta Deal: $3.0B over 5 years.

- Israel Infrastructure: ~$0.9B.

2. Funding the Future: The Prepayment Moat

Historically, scaling at this speed (4-5x CapEx growth) requires massive dilution or high-interest debt. However, NBIS has secured a unique financial structure:

- 60%+ of CapEx is funded by upfront customer prepayments.

- This de-risks the $16B-$20B CapEx guidance for 2026, as the "hyperscalers" are essentially financing their own capacity.

3. Valuation Scenarios for 2026

With a current market cap of ~$24B, the stock is trading at a significant discount to its 2026 targets.

| Scenario | 2026 ARR Target | P/S Multiple | Target Price | Upside |

|---|---|---|---|---|

| Base Case | $8.0 Billion | 8x | $253 | +166% |

| Bull Case | $9.0 Billion | 10x | $355 | +273% |

| Bear Case | $5.0 Billion | 6x | $119 | +25% |

4. Risks to Monitor

- Talent Scarcity: Scaling from 1,400 to 5,000 employees in 18 months is the primary execution bottleneck.

- Supply Chain: Dependency on NVIDIA Blackwell delivery schedules.

Verdict: At $95, NBIS offers one of the best risk-reward profiles in the AI sector. The market is pricing in a "Base Case" failure, creating a massive opportunity for long-term holders.