META vs. Google: Why Growth and Valuation No Longer Move in Tandem

In early 2026, a clear wedge has formed between Meta Platforms (META) and Alphabet (GOOGL). Despite being historical peers, their paths in the AI era have diverged significantly, offering a stark lesson in Valuation vs. Realized Growth.

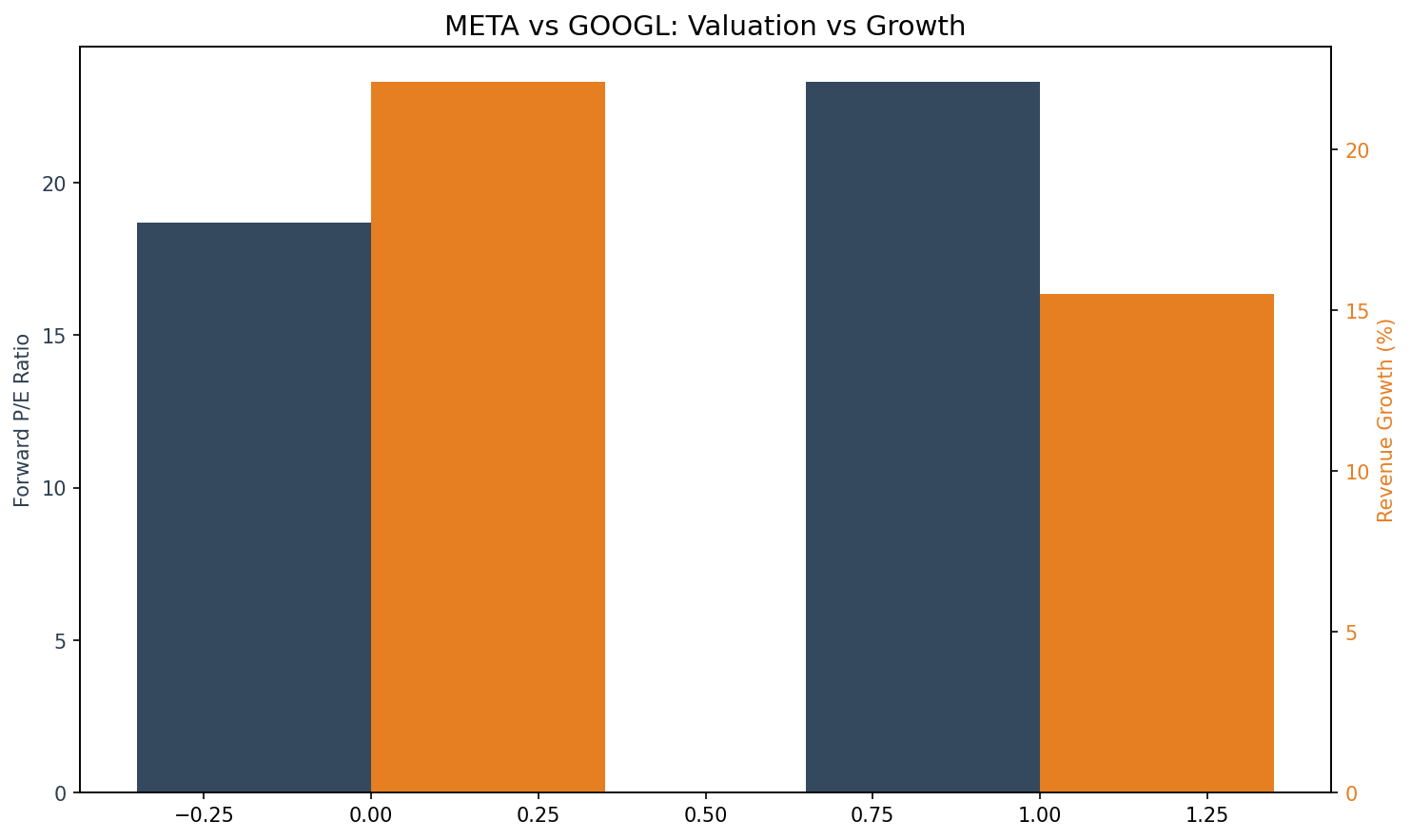

1. The Valuation Gap

Meta is currently trading at a Forward P/E of 18.7x, a deep discount compared to Alphabet’s 23.3x. Paradoxically, Meta is growing faster.

Why Meta is the "Value Play" in Tech:

- AI ROI Realization: Meta’s AI-driven recommendation engine is already boosting ad prices (+6%) and engagement (+18%).

- Operating Efficiency: Meta’s operating margin stands at a robust 41%, significantly higher than Google’s 32%.

2. Google's "Search Anxiety"

Alphabet’s technical breakdown—dropping below its 50-day and 60-day moving averages—reflects deeper structural fears:

- Search Cannibalization: The rise of AI-driven search (OpenAI, Perplexity) threatens the core "Link-based" ad model.

- Capex without Yield: While Google is spending $75B+ on Capex, the market has yet to see a "killer" AI monetization feature like Meta's ad optimization tools.

3. Technical Sentiment

Meta remains technically healthy, consolidating above key supports. Conversely, Alphabet is in a "dead zone," with RSI suggesting further downside to the $290 level before a meaningful bounce can be expected.

Investment Strategy

- Overweight META: The combination of 22% growth and an 18x Forward P/E is rare for a "Magnificent Seven" stock.

- Underweight GOOGL: Until the regulatory "Chrome-divestiture" risk is cleared and AI search monetization is proven, Alphabet remains a value trap.

Conclusion: For 2026, the market is rewarding Realized AI Revenue over Potential AI Power. Meta has delivered the former, while Google is still promising the latter.