Coinbase (COIN): Is the $160 Price Tag a Bearish Trap or a Value Opportunity?

Coinbase (COIN) has always been a "Volatilty Proxy" for the crypto market. However, at $162, the stock has decoupled from the fundamental progress the company made in 2024 and 2025. By using a Reverse DCF Model, we can "solve" for what the market currently believes about Coinbase's future.

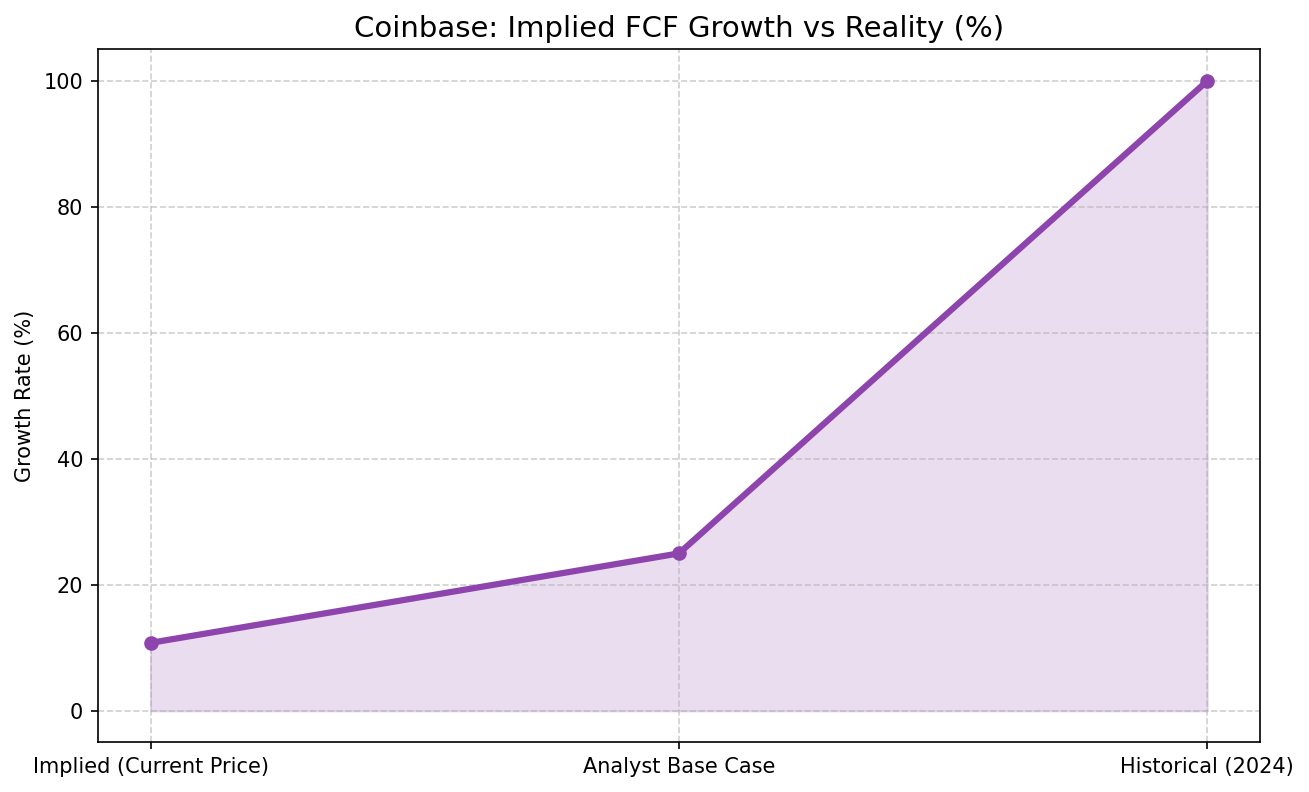

1. The 10.8% Growth Hurdle

Our model shows that at $162, the market only expects Coinbase to grow its Free Cash Flow by 10.8% annually over the next five years.

Why this is historically low:

- In 2024, Coinbase's revenue grew by over 100%.

- The market is essentially pricing COIN as a "Stagnant Utility" rather than a "Growth Tech" company.

2. The Multi-Billion Dollar Safety Net

Market participants often overlook the balance sheet. Coinbase holds $14.6 Billion in Cash and Equivalents.

- This represents nearly 33% of its current market cap.

- This cash provides an absolute floor for the stock, as the company can comfortably navigate years of low trading volume without existential risk.

3. Subscription & Services: The Hidden Gem

The shift from "Transaction Fees" to "Subscription Revenue" (USDC Interest, Staking, Custody) is the real story.

- Stable, non-volatile revenue now accounts for nearly 40% of total revenue.

- This "SaaS-like" revenue deserves a much higher multiple than the volatile trading fees.

4. Key Price Levels

- Support ($140 - $150): This is the "Strong Buy" zone where the market cap nearly matches the tangible book value plus cash.

- Resistance ($240): The first major hurdle for a valuation reset toward industry peers.

Final Thought

If you believe that Digital Assets will remain a permanent fixture of the global financial system, buying COIN at a 10.8% implied growth rate is one of the safest asymmetrical bets in the market today.

Rating: Strong Buy on Dips below $150.